Embed Size (px)

Citation preview

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 1/17

Financial Analysts JournalVolume 64 . Number 2

©2008, CFA InstituteF A J

Forecasting Fund Manager Alphas:The Impossible Just Takes Longer

M. Barton Waring and Sunder R. RamkumarExpected alpha from active fund managers can be forecasted — as long as one is mindful ofthe rulesof the zero-sum game of investing. Explicitforecasts are preferred over implicitforecasts becausesponsors can use explicit forecasts to build optimizedportfolios of managers with improvedmanagerweighting. To make explicit alpha forecasts, the investor combines two equa tions derived from thefundamental law of active management. Theelemental variables for the equationsare the sponsor'sestimate ofthe manager's "goodness" at beating the manager's benchmark, the sponsor's assessmentofthe sponsor's skill in estimating manager ability, the cross-sectional standard deviation of managerskill, portfolio breadth, implementation efficiency,expected active risk ofthe portfolio, andfees.

Forecasting is really hard, especial}}/ when it is about the future.

—Attributed to Niels Bohr^

We expect the premise of this article—thatone can and should forecast manageralphas—to be challenging for manyreaders. In our experience, many invest-

me nt professionals simp ly do not helieve that fundma nager alp has can be meaningfully forecasted.There is some irony in this reaction: Our observa-tion includes many, if not most, of those people

whose actual daily work is dominated by the taskof selecting and monitoring active fund managers.Selecting active fund managers and building

portfolios of them is an exercise in active manage-ment completely parallel to the work of conven-tional active fund man agers in selecting securities.The only difference is that the securities selected arenot " atomic" securities (the individ ual securities outof which fund managers build their portfolios) but"molecular" securities, the portfolios themselves,which are built up from many atoms. And when asponsor buildsa portfolio com posed of these molec-ular securities, the usual prescriptions for activeportfolio construction still apply. The objectivefunction for portfolio optimization is the same forthe sponsor as it is for the fund man ager: to maxi-mize expected portfolio alpha (net of fees) at anacceptable level of active risk. And som e forecastof future performance seems essential to either task.

M . Barton W aring is a managing director arid chiefinvestment officer for investment p olicy and strategy,emer i tus , /o r Barclays Global Investors, San Francisco.Sunder R. Rnmkuinnris a strategist with tjie Client Advi-sory Group at Barclays Global Investors, San Francisco.

As its point of departure, this article reliesheavily on Warijig, Whitney, Pirone, and Castille(2000) and Waring and Siegel (2003). These articlesdiscuss methods for building portfolios of activefund managers. Tlie Waring and Siegel article, inparticular, promised further improvements inthese forecasting methods. It is that promise thatwe mean to honor here.

Why Forecast Alphas?Althou gh m any sponsors try mightilyto avoid mak-ing specific forecasts of ma nager alphas, w e w ouldpoint out that the sponsor's holdings of active man-agers already contain embedded forecasts of thealpha for each manager. One simply needs a spe-cially fitted optimizer—a "reverse optimizer"—totease the alpha forecastsout.' Assume that the spon-sor thinks of its portfolio of managers as optimal,which in the context of active manager selectionmeans that the sponsor portfolio maximizes theexpected overall portfolio alpha at a given level ofoverall portfolio active risk.A reverse optimizer canback out the alpha forecasts that are required for theportfolio of mana gers to be optimal.

We have conducted this exercise with manyspon sors' portfolios, and w e are often su rprised bythe huge expected alphas that are implied by thelarge holdings of some of their active ma nagers (andparticularly by the large holding s of those man agerswho take a lot of active risk). But our main point isnot that the implied alpha forecasts are sometimesimpossibly large; our pointis that they arethere. One

March/April 2008 www.cfapubs.org 65

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 2/17

Financial Analysts Journal

cannot build a portfolio of active man agers w ithoutmaking alpha forecasts for each manager, eitherexplicitly or implicitly. Doing so explicitly is muchbetter. Explicit alpha forecasts can give the sponsormore meaningful guidance regarding which fundmanagers to hire, whether to fire or retain a man-ager, and how to weight the n^anagers in the port-folio. And such forecasts are essential to a well-optimized portfolio of fund managers.

Why Do Sponsors Resist Making ExpiicitAipha Forecasts ? Reluctance to make alpha fore-casts may reflect an un derlying skepticism thatanyfund managers are capable of delivering positivealpha consistently. After all, professionals in thesponsor organization would have been lecturedrepeatedly during their formal finance educationthat "th e mark et is efficient" so "you c an't beat themarket." Perhaps the real reason they continue tohire active fund managers is that their boards and

committees expect them to, not because theybelieve doing so will add value. If the sponsor'sboard or committee expects the sponsorto hire andretain active fund managers but the sponsorsecretly do es not believe that mana gers can be suc-cessfully chosenex ante, the sponsor might prefer aprocess that does not require any decision otherthan whether to hire or not hire the fund managerwh o appears to be "best" ina beauty contest paradeof applicants—which is today's dominant methodof selection. Someone with such a mind-set mightnaturally wish to avoid claiming much credit for

success or being held accountable for failure, andthe beauty contest process supports such an aspi-ration admirably! We could posit other explana-tions for current practice, bu t the conclusion is thesame: Practical results could be much improve d b yeither (1) carefully applying skill to the task ofmaking alpha forecasts or (2) giving up on the useof active management and defaulting entirely toinexpensive index funds.

As we will see, one can, in fact, build portfo-lios of securities and hire active fund managerssuccessfully—that is, with anex ante expectationof a positive expected alpha—given certain cond i-tions. The finance professors who taught us that"you can't beat the market" were only correct asfar as they went. Let's go farther.

The Two Conditions for Success in ActiveFund Management. Few finance professors wo uldassert toda y tha t markets are perfectly efficient.Most of them (as well as most practitioners) wouldagree that the ma rkets generallyapproach efficiencywithout attainingit. It is in the imperfections—thosebits of price-relevant information or know ledge that

are not yet efficiently and fully impounded inprices—that opportunit ies for above-marketreturns might be found.

But we must be careful here. Many investorsexpress the belief that one should always chooseactive fund m anagers (instead of index funds) inan ymarket that is inefficient. But this belief is seriouslyin error. Some inefficiency in the relevant mark et isa necessary condition for the expected success of activefund managemen t, hut it is nota sufficient condition;Even the most inefficient market imaginab le—say, a"frontier" emerging market country—is still a zero-sum game, in which the returns of all active playerssum to the return of the marketitself. (That is, anindex fund of that market will have mean perfor-mance, before fees and costs, with som e active play-ers beating it and some losing to it.) More thaninefficiency is required for active management tobeat an appropriate competing index fund.

What more is required for predictable, ratherthan random, success? The fund manager musteither know something that others in the market donot know orunderstand more clearly something thatis also known to others but not as well understoo dby them. The active manager has to have anedgeover the other players in the market. Eor short, wecall this edge "skill."^ Formally, w e refer to th is skillas a "posihve information coefficient."^ Formally,the information coefficient is the correlation of amanager's forecasts with subsequent realizations,and it is a forward-looking concept: A fund man-

ager has a positive information coefficient if themanager can, more often than not, predict whichsecurities will have positive alphas (and wh at theirmagnitude will be) during the upcoming period.*^

Such special skill is the ingredient for fundmanager success that is in limited supply and thatis also difficult for the sponsor to assess. Investorsdo not want to play the great zero-sum game—choosing to actively m anagea portfolio rather thanpassively hold its benchmark—unless they believethat they have skill at identifying securities or otherinvestm ent positions that will earna positive alpha

in the coming period.So, the Two Co nditions requ ired for a specific

active fund manager to have a positive expectedalpha are• some degree of inefficiency in the relev ant

market and• abov e-avera ge skill on the part of the fund

manager.The first condition is easy for most people to

accept. The second can be accepted as a generalpropo sition by m ost, in the sense thatsome manag-ers must have above-average skill or the Warren

66 www.cfapubs.org ©2008, CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 3/17

Forecasting Fund Manager Alphas

Buffetts of the world would bave no honor. But itcauses angst if we try to get specific: From a p opu -lation of tnanagers who obviously do not haveabove-average skill on average, how can one iden-tify which managersdo have special skill?

Let's turn to the perspective of the hiringsponsor.

The Two Conditions for Emptoying ActiveFund Managers. What must a sponsor believebefore deciding to hire active fund manag ers— thatis, if the sponsor wants to hire a portfolio of activefund managers having a collectively positiveexpected alpha?

First, the sponsor hasto believe that successfulactive management is, in the abstract, possible.Although traditionally this belief has been pooh-poohed ("you can't beat the market"), we hope wehave been persuasive in the prior section that thisis, in fact, possible (and we argue for it in greater

detail later). So, the sponsor must accept the first setof the Two Conditions as expressed in the priorsection, und er w hich one can believe that good fundmanage rs might, in fact, exist.A more intuitive wayto express this is that the sponsor must first believethat some "good" fund managers do exist.

Second, tbe sponsor h as to be ableto move fromthe general to the specific: It mus t believe thatit hasthe skill to idetitify fund managers that have skill—thatis, the skill to differentiate between the good, thebad, and the indifferent fund manager, before thefact.'' So, the key to success for spo nsorsis also skill.

Skill. In short, tw o very separate levels of skillare required: The sponsor needs to have skill atidentifying fund managers who have skill at pick-ing securities and other investment positions.

Across the unive rse of players, skill averages toa value ofzero. The average investor gets the marketretum, which is a way of summarizing Sharpe'swonderful 1991 article, "The Arithmetic of ActiveManagement," in which he so eloquently showedthat the market is a zero-sum game. More com-pletely, the marketis a negative-sum gam e, with thenegativity reflecting the necessary impact of feesand costs incurred in the effort of playing the gam e.

But not everybo dy is average! In fact, in nearlyany skill-based activity, whether it is buying stocksor figure skating, thereis a wid e distribution of skilllevels among the population engaged in the activ-ity. Most of us have recognized ever since somejunior high school teacher explained she was grad-ing "on the curve" that some few are destined toearn an A and equally few will earn anF, that morewill earn a B or a D, and that the greatest numberare going to get a C. The bell curve, or normaldistribution, d oes a great job of lending intuition to

the notion that some of us are more skillful thanothers, and it is logical to assume that this distribu-tion is a decent descriptor of skill or talent in anyendeavor—including active man agement.

Wh at does it mean to have skill in active man-agement? Because the average player in the ma rketsis fairly w ell educated and intelligent, the skill levelsneeded are those that stand out in a tough crowd.To be considered skillful in this particular senserequires more than merely being smarter than theaverage hu ma n being or even being more skillful asan investor than the general popu lation. To have anexpectation of being a successful active manager,one m ust ha ve skill that is above average relative tothe skill of others who are "playing the game" oftrying to beat the market. Thatis, one must be aboveaverage in an above-average dom ain. If active m an-agement were a zero-sum game, then perhaps halfof those actually playing (that is, of those thinkingthemselves good enoug h to give it atry) would have

sufficient skill. But because it is a negative-sumgame, only something less than half of the playerswill be skilled enough to win after covering theirfees and embedded costs (and to win by enough tojustify the additional risk taken on).

The good news for sponsors that plan to hireactive manag ers, how ever, is that skill levels do, infact, vary widely. The market is a mechanism bywhich the more skilled can profit at the expense ofthe less skilled. So, good players almost certainlymust exist, both at the fund manager level ami at thesponsor level. A sponsor with skill at identifying

fund man ager skill has a serious edge.Comparing Techniques for Building Port-

folios of Managers. Today's most common man-ager selection approaches almost never include anexplicit alpha-forecasting process. The wide ly usedbeauty pageant approach tries to pick the bestmanag er, but little or no effort is ma de to quantifyspecific expectations for future alpha (unless onegives credit to the effort to sort out future perfor-mance by studying past performance, a dang erouscredit to extend). Of course, there is a hop e tha t theman ager chosen will ata minimum outperform theappropriate benchmark.^ After all, staff members,committees, and boards do take their tasks seri-ously, and if the "best manager" from this processwere not even expected to outperform an indexfund, then one su ppo ses (or at least hopes) tha t then:ianager would not be chosen.

Not only is the list of mana gers selected impor-tant, but so are the weights given to these manag-ers. In today's practice, manager weights are oftendictated by the desire to fill out "style boxes," amethod that assigns weights based on the styles(i.e., multifactor beta characteristics) of the fimd

March/April 2008 www.cfapub5.org 6 7

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 4/17

Fir)ancial Ar}alysts Journal

managers. So, managers are selected in a series ofbeauty contests, and then the portfolio is built byinvesting in those managers in amounts sufficientto fill out each style box's requ ired weight.

In contrast. Waring et al. (2000) provided adifferent method. The authors extended the activeportfolio construction approach of Grinold andKahn (2000a) up one level—from the fund man-

ager's problem to the sponsor's problem. Theyshowed that the ideal portfolio of managers is anoptimized one that maximizes overall expectedalpha (summed across the managers) at a given or"acceptable" level of active risk (also taken collec-tively across the managers). To build such a port-folio, expected alpha mu st be specifically estimatedfor each candidate fund manager. The method hasbecome known as "manager structure optimiza-tion " (MSO)."''

Soon after those publications, Kahn (2000)show ed that in an ideal optim ized p ortfolio of man-

agers, manager weights, wlj ., would be propor-tional to the man ager 's expected alph a, a ^ ,,divid ed by expected active variance, co^ .:

COMgr(1)

Equation 1 is algebraically equivalent to saying thatthe total "bet"— thatis, the optimal m anager weighttimes the manager's active risk—is proportional tothe manager's expectedinformation ratio, IR :

The perspectives of W aring et al. and of Kahnshow—and for the same reason—that expectedfund manager alpha is one of the most importantdeterminants of the ideal weights of managers inthe portfolio.

So, it does not make sense to hire active fundmanagers simply because they are active—ever.And hiring active fund managers without makingand using explicit expected alpha forecasts for eachof them is definitely suboptim al. Moreover, not sur-prisingly, the expected alpha will also have animportant impact on the weight given to each man-ager selected.Thus, optimal portfolios of fund managersrequire specific estimates of expected und mana ger alpha.

Do Historical Alphas Help Forecast FutureAlphas? The regulator's required disclaimer tothe effect that "past performance is no guaranteeof future performance" is correct, but it can beovergeneralized to mean that historical datanevercontain any useful information. That interpreta-tion would not be true, but even so, with rareexceptions, whatever information does happen tobe in the data is extremely difficult to ferret outwith any confidence.^^

One m ethod of extracting information fromthe data might be to use a statistician's tools forseparating skillful from unskillful historical per-formance. A difference-of-means test (which p ro-vides the familiar ^statistic) could be used in anattem pt to reject the null hypo thesis tha t the histor-ical alpha of the fund manager has a zero mean(before fees). Few managers' data sets will "pass"such a skill test, however, because by construction,passing generally requires something like a95 per-cent confidence level.'^

This situation is a real challenge to the wide-spread p ractice of giving heavy w eight to historicalfund manager alpha. If one cannot claim with rea-sonable certainty that the fund ma nage r's mean his-torical alpha is significantly different from zero—ifit does not pass the f-test—the statistician hasa strictprescription for these sponsors:Simply throw thehistorical data away and completely disregard them when

considering the manager's future alpha. Only otherdata, most likely fundamental data, can be fairlyconsidered in this event.

The prescription is only slightly mo re helpfulifthe fund manager's datado pass the ^test. li a 95percent confidence interval is used, there is still a 5percent chance that the strong performance wassimply a random occurrence rather than the resultof skill. As we said, getting information out of his-torical alpha data isn't easy.

The best conclusion is that passing the f-testprovides only evidence of skill, no tproof. Therefore,

although the fact thata ma nager's historical alph ashave passed a f-test is surely admissible (in thetechnical sense) in the process of evaluating fundmanagers, it is by no means conclusive as to themanager's skillfulness. The sponsor should alsolook at fundam ental data.So, whether the data passa Ntest or not, historical data should be relied onmuch less than is found in current manager selec-tion practices.

Here is another way to look at the historicaldata issue: If real information in the historical datais so difficult to tease out th ata sponsor is not goingto be successful in the effort, then any portfolio offund managers constructed by the sponsor on thebasis of those data is simply going to have rand omperformance around the benchmark—that is, zeromean alpha before fees and costs and negativemean alpha after fund m anage r fees and costs. Aportfolio based on such data, without skill, is a"closet index fund"—and one with high fees andhigh trackingerror. It will deliverits beta, bu t it willonly overperform or underperform randomly; itsrealized alpha over time will simply be Brownianmotion—pure random ness with a negative bias.

68 www.cfapubs.org ©2008, CFA In stitute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 5/17

Forecasting Fund Manager Alphas

Such a portfolio, and sadly, it is the norm,creates the expectation that the efforts of the spon -sor will result in true added value. But, in fact, itconfuses n:iotion with forward progress. A spon-sor using historical data to project future alphacould reduce its active risk and improve after-feeperformance simply by moving to an all-indexedimplementation.

In contrast, if the portfolio of fund managers isassembled optimally, with skillful (after-fee) alphaforecasts that do not rely inappropriately on unin-formative historical (or other) data, it will have apositive expected alpha at the total portfolio level,a characteristic that index funds obviously cannothave. Such an outcome can be achieved only by asponsor that has and uses skill in ideritifying fundmanager skill. There is no formula; there is norecipe; there are no shortcuts.

Skill necessarily implies theexercise of informedjudgment. So, at some point, someone must make a

claim of skill and be prepared to try to deliver onthat claim. This person or group of persons needsto step up to the plate, make an informed butjudgm ent-based forecast for the alpha s of the can-didate fund managers, and be accountable at thetotal portfolio level for being more right thanwrong . We now present a methodology for sensi-bly approaching this task.

Forecas ting Fund Manager AlphasTwo useful relationships are described in the activemanagement literature that can be used to guidethe search for a method of forecasting alphas. Thefirst is the fundam ental law of active m anage men t,which we shorten to the "fundamental law." Thesecond is often called the "forecasting equation."Both are attributed to Grinold (1989,1994).!^

Not surprisingly, both of these relationshipsare closely tied toskil], and given the two levels ofskill required in our problem, we'll find this to beuseful. W e'll review these relationships in the con-text of this paper 's task and then look at how to usethem, or variations of them, to formally forecastfund manager alpha.

Relationship No. 1: The Fundamental Law.The fundamental law is most often stated in a formthat shows the relationship of a fund manager'sexpected portfolio information ratio to certain of itskey determinants. The expected information ratiois the ratio of the portfolio's expected alpha, a, tothe portfolio's p ure active risk,to. According to thefundamen tal law, the expected information ratio isa function of the inform ation coefficient, /C, and ofselection breadth, Br. In mathematical notation(with the expectations operators omitted from thevariables to simplify the display), the law is

(3)

We have used a separator in the subscript n ota-tion, as in /Cj^,Tri M PP^'^ ^^^P ^^ keep track of, first,which playe r itis (the fund man ager or the sponsor)

that the estimate applies to and, second, whichplayer is making the estimate or is responsible forthe resu lt. This ex ample, /C/ ^prlM ef n^eans "theinformation coefficient of the manager in the viewof the manager" (a self-assessed informationcoef-

ficient). If it were /^C^erlSwon' i* would mean "theinformation coefficient of the manager in the viewof the sponsor" and clearly could differ from/CjviprlM i'i- Ditto for other variat ions.

In plain languag e,then. Equation 3 reads: "Theexpected inforn^ation ratio of a fund manager'sactive portfolio, in the view of the m anager, equalsthe expected information coefficient, or skill, of themanager (as assessed by the manager) times thesquare root of expected breadth of the portfolio."

In Equation 3, the information coefficient rep-resents the fund manager's skill at forecasting thereturns of the individual securities that may go intohis or her portfolio. It is more formally defined asthe expected correlation coefficient between fore-cast returns and subsequent realized returns.

Breadth, Br, represents the num ber of indepen-dent (uncorrelated) bets that the fund managermakes in the measurement period—usually,a year.It is a measure of the extent to which active bets arediversified or, more precisely, the extent to whichforecasting skill is applied broadly among securi-ties (or other investment positions). The breadthterm in the fundamental law implies that the mostconsistently successful fund managers are thosewho apply their forecasting skill widely over alarge number of independen tbets. As Grinold andKahn noted, the fundamental law boils down to amandate to "play often, and play well."^^

Although the original fundamental law wasderived in the absence of constraints, real-worldportfolios are rarely unconstrained. Grinold andKahn (2000a) demon strated that the long-only con-straint severely limits fund managers' abilities toimplem ent their insights and results ina significantperformance drag when such portfolios are com-pared with a similarly optimized but uncon-strained portfolio. Thus, the fundamental law canbe expanded to include an addition al term, referredto as the "transfer coefficient," that reflects the p er-formance drag or inefficiency resulting from con-straints.^^ Stated another way, the transfercoefficient is the ratio of the info rmation ratio of the

March /April 2008 www.cfapubs.org 69

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 6/17

Financial Arialysts Journal

portfolio to the information ratio of a portfoliobased on identical information but implementedwithou t any constraints.

So, the fundamental law, modified to incorpo-rate the transfer coefficient, TC, and subscripted toapply to its ordinary perspective, that of the fundmanager, is

(4)

Mgr\Mgr yj^^'Mgr ^^Mgr •

We are interested in forecasting alphas, so werestate the fundamental law to focus on theexpected alpha term by multiplying both sides ofEquation 4 by expected active risk (movingoj to theright side of the equation);

So far, the point of view has been that of themanager, b ut the sponso r has not been forgotten. Wewill come back to the spo nsor's role in a mom ent.

Relationship No. 2: The ForecastingE q u a t i o n . The forecasting equation is

Equation 6 means that the expected alpha of a secu-rity in the view ofa portfolio mana geris the productof the skill of the manager, times the active risk(standard deviation of residuals) of the security,times the z-score of the security—all as assessed bythe manager. Grinold's purpose in developing thisrelationship was to help fund managers readilyform forecasts of alpha for individ ual securities (notalphas for the fund manager po rtfolios themselves,consisting of many securities).

The z-score is a standardized variable thatreflects the fund manager's evaluation of the"goodness" of a security (or in the application wedescribe next, the sponso r's evaluation of the extentof the fund manager's skill). Mathematically, the

2-score has a normal distribution with a mean of0and a standard deviation of1. Thus, "buys" wouldbe assigned a positive z-score and"sells"a negative2-score. A 2-score of 1, for example, suggests thatthe security is believed to be1 standard deviationbetter than average; it would thus be better thanroughly five-sixths of all stocks being assessed bythat fund manag er. Rarely wo uld a security earn az-score of 2, and a 3 would be a one-in-a-thousandevent. If a fund man ager had n o view on a security,the manager would assign it a 0 2-score, implyingno alpha expectation.

The security's residual or pure active risk{"Sfv I M-^r) s the standa rd deviation of the security'smonthly or annual alphas overtime. The more vol-atile the security's alpha, the greater the opportu-nity to profit from its price moves—for ex amp le, bybuying it on its upsw ing an d selling it on its dow n-swing. Thus, a higher volatility translates into ahigher expected alpha, for a given level of skill.

This forecasting formula is Bayesian, inessence. It begins w itha raw forecast—that the secu-rity alpha is the product of the standard deviationtimes the 2-score assigned to the security by themanag er—thus, for the moment, treating this resultas if it were a perfect forecast. The formula thenmodifies this raw forecast, correcting it back tow ardthe null hypothesis (or "prior") that the uncondi-tional forecast is zero by multiplying it by the skillterm—the ma nag er's own information coefficient.

The "Aipha-Buiider" Forecasting Frame-work. We now have the building blocks for a verycomplete forecasting framework and can tie themtogether. A prior article (Waring and Siegel 2003)provided a preliminary approach to forecastingalpha co nsisting simply of the Grinold forecastingequation with m inor adjustments to adap t it to theproblem of sponsors assessing the expected alphaof ma nagers:

(7)

Equation 7 reads: "Expected alpha for a fund man -ager, in the view of the sponsor, is equal to thespon sor's skill times the fund ma nage r's expectedlevel of active risk, 03^^,,., times the unit normal2-score, z^g,. \ ^pou • assigned to the fund m anag er bythe sponsor as an expression of the sponsor's viewof that fund ma nag er's skill level, minus fees."

In practice, this forecasting equation seemed toproduce reasonable results when used with thetechnology for optimizing fund manager structureand bud geting fund m anager risk described earlier.Yet, we were convinced that it could be improved.Eor one thing, this formula clearly does not explic-itly incorporate the two levels of required skill. Foranother thing, it does not incorporate other know nimpo rtant variables, such as fund m anage r breadthand the transfer coefficient. We anticipated furtherdevelo pm ents; this article is the result.^^

The first major improvement is that wedirectly evaluate the fund manager's forecastingskill, the information coefficient, rather than themanager's alpha as we did in the prior effort. Andsecond, we make it so that whenever a sponsorassesses fund manager skill, the methodologyrequires a self-assessment of the sponsor's skill at

70 wvvw.cfapubs.org ©2008, CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 7/17

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 8/17

Financial Analysts Journal

We see many sponsors attemp t to reduce theirselection efforts to a repeatable process or "recipe ."An estimate of expected alpha, explicit or implicit,is likely to be worthless, however, if it can bereduced to a recipe. That is, skill and judgmenthave to be in the mix somewhere, and the use of arecipe inherently suggests that one is avoiding theuse of skill or judgment.

We have found percentiles to be more intuitivefor many sponsors than raw 2-scores when evalu-ating fund managers. Because z-scores are inher-ently normally distribu ted, a percentile rank can beeasily translated into a 2-score by using standardprobability tables. Table 1 indicates that a fundmanager thought by the sponsor to be at the 84thpercentile can be understoo d by the analyst to havean assigned 2-score of+1 whereas a fund managerassigned a 98th percentile rank can be interpretedas having a 2-score of +2.

Table 1. Relationship between Fund Managerz-Score and

Percentilo Rank

27

16

3150698493

98

Percentile RankManager z-Score

-2.0-1.5-1.0-0.5

0.00.51.0

1.5

2.0

Variability of fund manager skill (G

This variable represents the cross-sectional stan-dard deviation of skill (where skill is expressed asinformation coefficient) across the universe of gen-erally similar active fund man agers. Intuitively, onecan understand that the greater the variations infund man ager skill, the greater the impa ct of spon-sor skill in selecting a good manager—thus, thegreater the spons or's alpha expe ctations (even afterbeing pared back by the action of the other term s of

the forecasting approach).There is no direct way to observe this standard

deviatio n, but one can back into it inferentially. W ebelieve that an estimate of 0.07 for ic^/,,.is sensible,and w e note that this value is consistent with large-capitalization U.S. equity mutual fund data; we arecurrently using it and have found that it givesreasonable estimates. (As shown in the first exam-ples in the next section, this value produces aninformation ratio of 0.50 for an active equity fundmanager with an S&P 500 Index benchmark at anactive risk level of 5.0 percent, which is typical of a

traditional active manager who is at the first quar-tile of performance.^*^) Obviously, there is someroom to hope for improvement in this estimate,particularly when dealing with managers of assetclasses other than large-capU.S.equities. Until bet-ter data are available, how ever, w e will use the 0.07estimate for most benchm arks.

Sponsor skill (lCspan\Spo,i)- 'This variablemay be the most difficult to assess of the seven inthe model; itis certainly one ofthe two m ost difficultto estimate (the other being th e 2-score).ICg,,^^,, | g,,^,,,the information coefficient of the sponsor in thespon sor's own view, is a quantification of the spon -sor's skill in picking good active fund manag ers—or, more precisely, of the sponsor's skill in assessingthe fund managers' skill.iCsp^,,\s,,^,j - 0 implies abefore-fee expected alpha of zero, regardless of howhigh a 2-score the sponso r m ay hav e given a partic-ular fvmd manager: It means that the sponsor itself

believes that its estimate of the m ana ger's z-score isno good and should not be used (so it will not beused because multiplying by ICspon\Spon = 0yields a before-fee expected alpha of zero, nomatter wh at the other inputs are). In other words,no matter how good the sponsor thinks a fundmanager is, if the sponsor's judgments are notbelieved—even by the sponsor—to have any pre-dictive ability, they are irrelevant and the sponsorshould not expect any alpha.

Estimating sponsor skill is a problem inself-assessment. It is difficult to do in any completely

satisfactory manner because the board,staff, andconsultants involved in the process rarely have thedata needed to demonstrate their ow n statisticallysignificant performance. In fact, the more com-pletely they understand the problem, the moremodest they may be in claiming special skill. Butthese people may be precisely the ones who havethe greatest chance of winning the game.

We are not going to tell anyone how to estimatehis or her own skill, but we would start by notingtha t if a given sponsor is playin g the active man agerselection game, then it has also made an impliedpositive estimate of its skill,ICc;„^,„\5„^,„. The gameleaves the sponsor no room to be troubled by itsinability to be certain abou t its own skill. The zero-sum gam e of active management requires that onebelieve in oneself. Everyone and every group thathas ever considered engaging in a sporting eventor other contest has faced the same uncertainty inwhat are also usually zero-sum games, yet thegames are never short of players. The zero-sumgame of active management, as for most othergames, requires only that one believe in oneself ifone is going to play, and this is expressed as apositive IC.

72 www.cfapubs.org ©2008, CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 9/17

Forecasting Fund Manager Alphas

Rather than estimate sponsor skill directly,some might prefer to use a boundary condition tosubstitute for it. For example, a sponsor might say,"We estimate that in order to have a portfolioexpected alpha that is positive and valuable, afterpaying fund manager fees and experiencing activefund manaeement transaction costs, we need aninformation coefficient of at least 0.33.'

Such a boundary is not in itself a proper esti-mate of sponsor skill—far from it—but it representsa lower limit on the amount of skill a sponsor musthave, given the prior intent to hire active managers,in order to be successful. The sponsor may welldecide that its skill level is higher than the mini-mum level required to make the hiring of activemanagers a rational choice. But if the lower bounditself is used by the staff as its estimate of^^5pon\Sf'pii' using the alpha-builder process willhave the virtue of organizing fund managerexpected alpha estimates in a form that is consistent

from one manager to the next, putting them on aplaying field leveled for costs, risks, breadth, andthe transfer coefficient. Using the lower bound is astart, from which one can proceed to more sophis-ticated estimates if one chooses. ^

Many sponsors will prefer to express their self-estimate of skill as an expected future "win rate"rather than an information coefficient. For example,a sponsor might say, "I think about two out of everythree fund managers that we pick, or 67 percent, willoutperform." This estimate can be used to approxi-mate the information coefficient. " Win rates (whichwe will designate p, the probability of success)range from 0 percent to 100 percent; informationcoefficients, being correlation coefficients, rangefrom -1 to +1. We can convert the win rates to theinformation coefficients by using the following:

^^SponlSpon= 2 p - l . (12)

Thus, if the sponsor anticipates being right 67 per-cent of the time, IC^^^,, \ g,,,,,, is fairly approximatedas 0.34; if the win rate is 50 percent, then, of course,/Cgp,, I spo,, is 0 .00.Table 2 lays out this relationship.In the next section, we examine the impact of vari-ous information coefficients.

Table 2. Estimating Sponsor SkillSponsorSuccess

ProportioniP )

Sponsor Skill'"-Sjiaii 1 Spun)

0%20406080

100

-1.0

-0 .6-0 .2

0.20.61.0

Any degree of error introduced by misestimat-ing the sponsor's information coefficient will, ofcourse, affect the results. An obvious example isthat a sponsor mistakenly claiming an informationcoefficient of 0.30 but having a true informationcoefficient of 0.00 will achieve a return that is ran-domly distributed around the benchmark with amean of zero, minus fees and costs.

Furthermore, low sponsor information coeffi-cients favor low-fee and low-tracking-error manag-ers. As the sponsor's own information coefficientapproaches zero, the net expected alpha for themanager derived in our framework will begin toapproach manager fees. In this case, any opti-mizer will simply pick the managers with the low-est fees and lowest active risk—that is, index funds.This result should not be a surprise. A sponsor withno confidence in its ability to pick managersshouldn't really be investing in active managers.

Anyway, if a sponsor is going to play the greatzero-sum game of active manager selection, andplay to win, the sponsor must take responsibilityfor the critically important self-assessment embod-ied in its estimate of /Cg , ,, 15 , ,,,. Without doing so,and coming up positive, a sponsor simply cannotjustify hiring active managers.

Fund manager breadth (fi'A/g,.|5'/,y,,)- Breadth isthe number of statistically independent investmentbets made by an active manager each year. Greaterbreadth results in more diversification of the resid-ual risk from the active management effort and, all

else being equal, improves the consistency (reducesthe standard deviation) of the fund manager's per-formance. If that fund manager has skill, such thathis expected alpha is a positive number, then as thestandard deviation of the residual risk decreases,the percentage of the time that the fund manager'srealized alpha is above zero increases. In the sameway, the house in Las Vegas operating a roulettewheel, with its tiny built-in house advantage, isalmost completely safe if it handles a million betsfor a dollar each but is taking an unacceptably highrisk by handling one bet for $1 million.

Despite the simplicity of the concept, estimat-ing breadth in practice is not an exercise in precision,whether the estimate is being made by the manageror the sponsor. (The sponsor has even more diffi-culty than the fund manager in accurately estimat-ing the manager's breadth because the sponsor lacksaccess to full information about the portfolio's con-struction and the reasoning behind it.) Few forecastsare completely independent, and many (or most)are highly correlated. An active fund managerbenchmarked to the S&P 500 might hold all 500stocks in her portfolio and might tum the portfolio

March/April 2008 www.cfdpubs.org 73

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 10/17

Financial Analysts Journal

over 200 percent per year, which would imply thatshe has made 1,000 independent decisions. Butbrea dth for this n:Tanager could easily be m uch lessthan 1,000 if the forecasts were driven by certaincommon factors and , therefore, are correlated—as isLikely to be the case most of the time. For example,fund managers may assign higher expected alphasto stocks that have don e well recently(a momentumfactor) or stocks in the technology industry (anindustry factor). In these examples, the fund man-ager is essentially m aking only one informed bet (onmom entum or on an industry) despite appearing tofollow all the stocks in the benchmark.

Nonetheless, a safe point for the sponsor tostart the estimation process is to assume tha t mostfund managers' breadth is proportional to theprodu ct of the num ber of securities being activelyevaluated t imes the annual turnover.^ ' ' Butbecause of the number of signals used and theircorrelation, as discussed, this proportio n is likelyto be considerably less than 1. And the sponsorshould certainly refine any such rough estimate hyusing any information it can obtain regardin g thefund ma nage r's signals and portfolio constructiontechn ique s. The goal is to mean ingfully differen-tiate the fund managers from each other based onwhat they actually do.

The transfer coefficient (TC^^.^Sfm,)•T'hetransfer coefficient, as already noted, reflects theimpact of constraints on the portfolio's perfor-mance. The most binding constraint on typicalportfolios is the no-shortin g restriction. It severelylimits a fund ma nage r's ability to implem ent neg-ative views on securities and reduces the alphapotential of the portfolio.

We can estim ate the transfer coefficient of long-only equity portfolios by using an empirical resultpresente d in Grinold and Kahn (2000b). They con-ducted simulations to examine the informationratios of optimal portfolios based on the same infor-mation but implemented with and without thelong-only constraint. They measured the transfercoefficient related to the long-only constraint,

denotedTCL,,,,^,^,,/,,,

at varying risk bud gets an d forvarious benchmarks, and they found that theirresults fit the following polynom ial expression w ell:

TCLongOnly1

CO,

1+0),(13)

where Y(N) = (53 + N)'^'^'^(it is simply a calibratingfactor that they estimated empirically) andN is thenumber of securities in the benchmark portfolio.

Equation 13 demonstrates that the two factorsthat act to reduce the transfer coefficient most in along-only portfolio are(1) a larger numb er of stocksin the benchmark (which reduces the averageweight of the stocks and thu s the amount by whichthe manager can express a negative view by notholding a stock) and (2) greater active risk in theportfolio (which increases the size of optimal activepositions, which are then increasingly constrainedif negative). The most "efficient" funds, then—those with the highest transfer coefficients—will bethose with low active risks that are operating infairly narrow markets.

Active risk ((X)M^,^spon)-The fund m anag er ' sactive risk, or tracking error, represents the annua l-ized standard deviation of the fund manager'sresiduals, or alph as. Ifa positive value is assumedfor manag er skill, higher active risk translates in toa higher expected alpha. (The relationship is notlinear, however, for long-only portfolios becauseportfolios w ith higher active risks are also penalizedby having lower transfer coefficients.)

Active risk is perhaps the easiest variable toforecast. It is much m ore stable than alph a and canbe reasonably estimated from historical data (usu-ally with an acceptable degree of error, but thereare exceptions). At the same time, the sponsormust be sure that the active risk it measures isestimated relative to the appropriate benchmark,or beta (or, usua lly,a mix of m ultifactor beta s), onethat represents the fund manager's opportunityset and process.

Many active fund managers have systematicstyle biases (va lue, small cap, etc.) that differ fromtheir stated benchmarks. A simple style analysiscan identify the fund manager's actual averagestyle during the study period, and active riskshould be measured relative to this bench ma rk if ithas been relatively stable. Doing so provides for aclean separation of the beta and the alpha expo-sures and ensures that the sponsor is focusing onthe "pur e" alpha and p ure active risk (Waring andSiegel 2003).26

Fees {Feesf^f^,.^-^^,^,,,).U l t i m a t e l y, r e t u r n s n e tof fees represent the true value added by the fundmanager, so the sponsor should measure andaccount for fund manager fees somewhere in theprocess. Even a fund manager with skill will addno value to the sponsor if his fees are equal to orhigher than his expected alpha. For this reason,note thatZi^^^\ g,,,,,, is evaluated ona before-fee basisin our formulation; fees are then subtracted explic-itly by using a separate fee term.

74 www.cfapubs.org ©2008, CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 11/17

Forecasting Fund Manager Alphas

ExamplesTo dem onstra te the alpha-forecasting framework,we first consider examples th at illustrate the impor-tance of sponsor skill by comparing the alphaexpectations for sponsors with varying abilities inpicking good fund managers. Then, we considerexamples that explore the effects of the transfer

coefficient and of breadth.

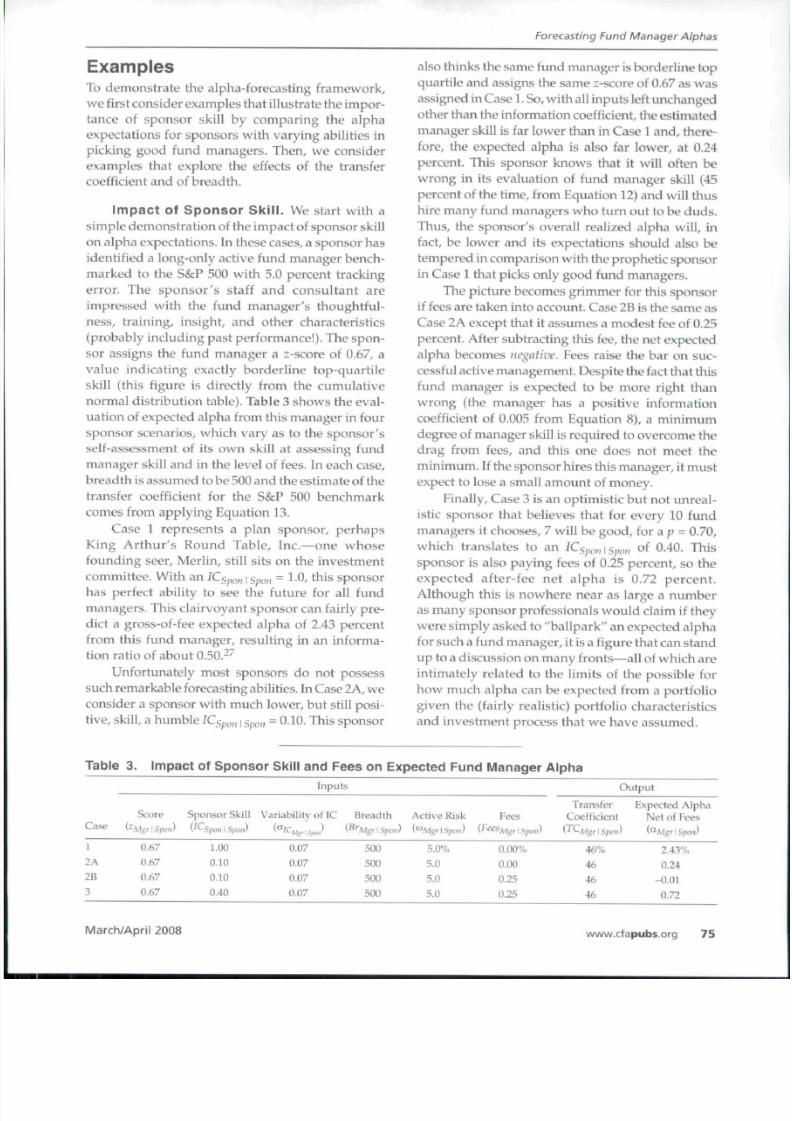

I m p a c t o f S p o n s o r S k i l l . We start with asimple dem onstrati on of the impa ct of sponsor skillon alpha expectations. In these cases, a sponsor ha sidentified a long-only active fund manager bench-marked to the S&P 500 with 5.0 percent trackingerror. The sponsor's staff and consultant areimpressed with the fund manager's thoughtful-ness, training, insight, and other characteristics(probably including past performance!). The spon-sor assigns the fund manager a z-score of 0.67, avalue indicating exactly borderline top-quartileskill (this figure is directly from the cumulativenormal distribution table). Table3 shows the eval-uation of expected alph a from this m anager in foursponsor scenarios, which vary as to the sp onso r'sself-assessment of its own skill at assessing fundmanager skill and in the level of fees. In each case,breadth is assumed to be500 and the estimate of thetransfer coefficient for the S&P 500 ben chm arkcomes from applying Equation 13.

Case 1 represents a plan sponsor, pe rhapsKing Arthur's Round Table, Inc.—one whosefounding seer. Merlin, still sits on the investmentcommittee. With an ICgpo,,| s p,, = 1.0, this sponsorhas perfect ability to see the future for all fundmanagers. This clairvoyant sponsor can fairly pre-dict a gross-of-fee expected alpha of 2.43 percentfrom this fund manager, resulting in an informa-tion ratio of about 0.50.^^

Unfortunately most sponsors do not possesssuch remarkable forecasting abilities.In Case 2A, w econsider a sponsor with much lower, but still posi-

tive, skill, a humble /Csj,,wI

Span = O-^O- This sponsor

also thinks the same fund mana geris borderline topquartile and assigns the same 2-score of0.67 as wasassigned in Case 1.So, with all inputs left unch angedother than the information coefficient, the estimatedmanager skill is far lower than in Case1 and, there-fore, the expected alpha is also far lower, at 0.24percent. This sponsor knows that it will often be

wrong in its evaluation of fund manager skill (45percent of the time, from Equation 12) and will thushire many fund managers who tum out to be duds .Thus, the sponsor's overall realized alpha will, infact, be lower and its expectations should also betempered in comparison w ith the prophetic spon sorin Case 1 that picks only good fund man agers.

The picture becomes grimmer for this sponsorif fees are taken into account. Case2B is the sam e asCase 2A except that it assum es a m odest fee of 0.25percent. After subtracting this fee, the net expectedalpha becomes negative. Fees raise the bar on suc-cessful active managem ent. D espite the fact that thisfund manager is expected to be more right thanwrong (the manager has a positive informationcoefficient of 0.005 from Equation 8), a minimumdegree of manag er skill is required to overcome thedrag from fees, and this one does not meet theminim um. If the sponsor hires this manager, it mustexpect to lose a small am ount of money.

Finally, Case 3 is an optim istic but n ot u nreal-istic sponsor that believes that for every 10 fundman agers it chooses,7 will be good, for a p - 0.70,which translates to an lCspon\Spon of 0.40. Thissponsor is also paying fees of 0.25 percent, so theexpected after-fee net alpha is 0.72 percent.Although this is nowhere near as large a numberas many sponsor professionals would claim if theywere simply asked to "ballpark" an expected alphafor such a fund manager, itis a figure that can stan dup to a discussion on m any fronts—all of whic h areintimately related to the limits of the possible forhow much alpha can be expected from a portfoliogiven the (fairly realistic) portfolio characteristics

and investment process that we have assumed.

Table 3. Impact of Sponsor Skill and Fees on Expected Fund Manager Alpha

Case

1

2A

2B

3

Scorey~Mgr\ Spon'

0.67

0.67

0.67

0.67

Sponsor SkillV^Spoti 1 Spon'

1.00

0.10

0.10

0.40

Inputs

Variability of !C

0.07

0.07

0.07

0.07

Breadth^''MgriSro,,)

500

500

500

500

Active Risk

5.0%

5.0

5.0

5.0

Fees^'"'^MxrlSpo,,)

0.00%

0.00

0.25

0.25

O u t p u t

TransferCoefficient

(I ^Mgr\Spoil)

46 %

46

46

46

Expected AlphaNet of Feesi^MgrlSfWii)

2.43%

0.24

-0.01

0.72

March/April 2008 www.cfapubs.org 75

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 12/17

Financial Analysts Journal

These cases throw lighton the importanceofskill in active management. Although sponsors andfund managers are tempted to make overly opti-mistic alpha forecasts(3 percent and 4 percent fore-casts of expected alpha will often be casuallybandie d a bout), actual realized retu rns for the port-folio of fund managers seldom reach such high

levels. Skill levels needto be considered w hen set-ting expectations but usually are not. Invariably,expectations become more modest when sponsorsare fully informed by following the alpha-builderforecasting process that fully incorporates skill esti-mates and other imp ortant variables.

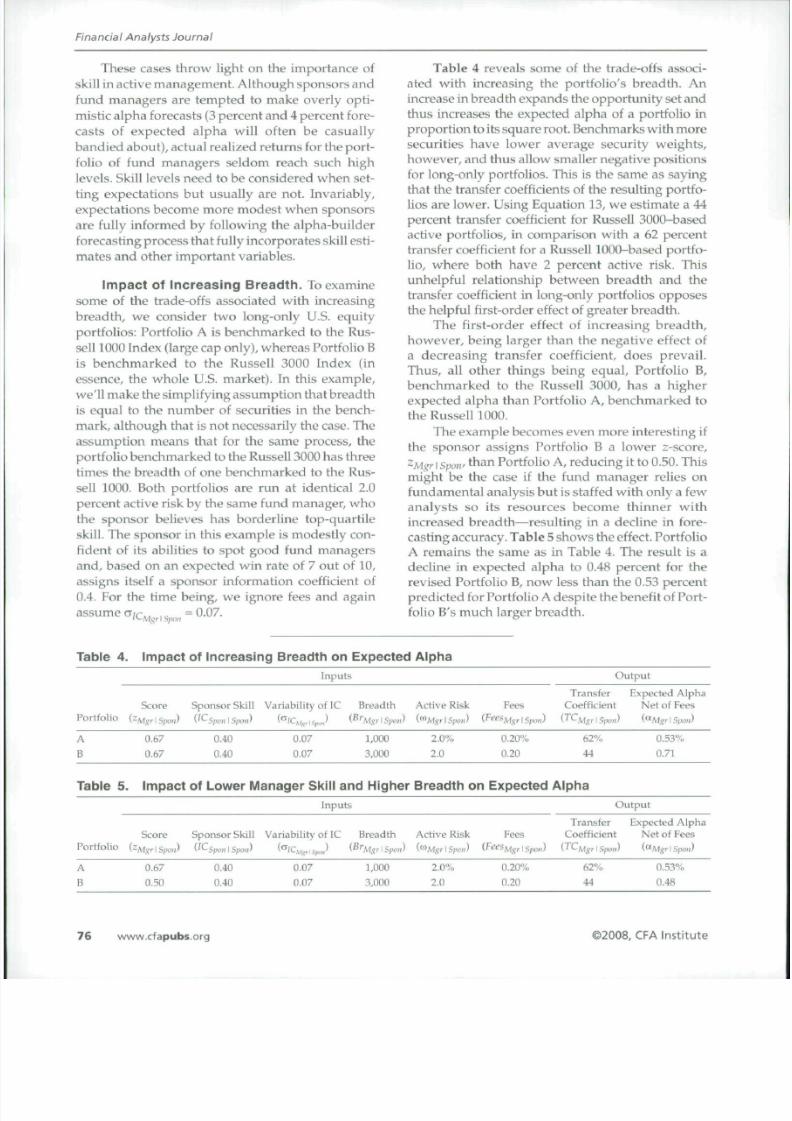

Impact of Increasing Breadth. To examinesome of the trade-offs associated with increasingbreadth, we consider two long-only U.S. equityportfolios: Portfolio Ais benchmarked to the Rus-sell 1000 Index (large cap only), whereas PortfolioB

is benchmarked to the Russell 3000 Index (inessence, the whole U.S. market).In this example,we'll make the simplifying assum ption that breadthis equal to the number of securities in the bench-mark , although that is not necessarily the case. Theassumption means that for the same process, theportfolio benchm arked to the Russell3000 has threetimes the breadth of one benchmarked to the Rus-sell 1000. Both portfolios are run at identical 2.0percent active risk by the same fund manager, w hothe sponsor believes has borderline top-quartileskill. The spon sor in this example is modestly con-

fident of its abilities to spot good fund managersand, based on an expected win rate of 7 out of 10,assigns itself a sponsor information coefficientof0.4. For the time being, we ignore fees and again

assume Mgr \Spmi=0.07.

Table 4 reveals some of the trade-offs associ-ated with increasing the portfolio's breadth. Anincrease in breadth ex pands the oppo rtunity set andthus increases the expected alpha of a portfolio inproportion to its square root. Benchmarks with m oresecurities have lower average security weights,however, and thus allow smaller negative positionsfor long-only portfolios. Thisis the same as sayingtha t the transfer coefficientsof the resulting portfo-lios are lower. Using Equation13, we estimate a 44percent transfer coefficient for Russell 3000-basedactive portfolios, in comparison with a 62 percenttransfer coefficient for a Russell 1000-based portfo-lio, where both have 2 percent active risk. Thisunhelpful relationship between breadthand thetransfer coefficient in long-only portfolios opposesthe helpful first-order effectof greater breadth.

The first-order effect of increasing breadth,however, being larger than the negative effect ofa decreasing transfer coefficient, does prevail.Thus, all other things being equal. PortfolioB,benchmarked to the Russell 3000, has a higherexpected alpha than Portfolio A, benchmarkedtotheRusseinOOO.

The example becomes even more interestingifthe sponsor assigns Portfolio B a lower z-score,^Mer I Spoil' than Portfolio A, reducin git to 0.50. Tliismight be the case if the fund manager reliesonfundam ental analysis but is staffed with o nly a fewanalysts so its resources become thinner withincreased breadth—resultingin a decline in fore-casting accuracy. Table 5 shows the effect. PortfolioA remains the same as in Table 4. The result is adecline in expected alpha to 0.48 percent for therevised Portfolio B, now less than the 0.53 percentpredicted for PortfolioA despite the benefit of Port-folio B's much larger breadth.

Table 4. impact of Increasing Breadth on Expected A lpha

Portfolio (

A

B

Table 5.

Portfolio (

A

B

Score

0.67

0.67

Impact

Score^Mgr\ Spoil)

0.67

0.50

Sponsor Skill

i^^Spon 1 Spim)

0.40

0.40

Inputs

Variabili ty of IC

0.07

0.07

Breadth

1,000

3,000

of Lower Manager Skill and Higher

spon sor Ski lly'^bpoii \ Spoil)

0.40

0.40

Inputs

Variability of IC

0.07

0.07

Breadth

1,000

3,000

Active Risky^'^Mgr \ Spoil) V

2.0%

2.0

Breadth on

Active Risk

2.0%

2.0

Fees

0.207o

0.20

Expected

Fees

0.20%

0.20

Ou tpu t

TransferCoefficient

( ' *~-Mgr 1 Spoil'

62 %

44

Alpha

Expected AlphaNet of Fees

0.53%

0.71

O u t p u t

TransferCoefficient

C^CMgr \ Spoil)

62 %

44

Expected AlphaN e t of Feesi^Mgr 1 Spoil)

0.53%

0.48

76 www.cfapubs.org ©2008, CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 13/17

Forecasting Fund Manager Alphas

Therefore, increased breadth is useful only ifthe fund manager can sustain forecasting accuracyand intensity over a larger universe of securities—that is, if the increased breadth is, in fact, beingused effectively.

ConclusionThe ability to forecast expected alpha is one of thekeys to successfully employing active fund man-agers and deserves much more attention by spon-sors. Sponsors need to proactively forecast alphato ensure that their portfolios of fund managersare not merely random collections of past winnersand losers.

Forecasting alpha is hard, but it can be done. Thealpha-builder framew^ork described here helpsorganize the effort logically. It identifies the vari-ables that affect expected alpha, thus breaking upthe estimation problem into pieces that are easierto estimate than fund manager skill taken as aVi'hole. These variables, including sponsor informa-tion coefficient, active risk, breadth, and the trans-fer coefficient, are within the sponsor's estimationgrasp. Certainly, alpha estimation cannot be donewithout grappling with estimating these variablesat some level.

We have provided a rational means for scal-ing the two most difficult inputs, fund managerskill and the plan sponsor's skill at selecting fundmanagers, and incorporating these estimates withother important factors, such as active risk levels,breadth, fees, etc. The approach is reassuringlyfamiliar, in that it is based entirely on two bits ofcomfortably well-accepted alpha-forecastingmethods—the Grinold forecasting equation andthe fundamental law of active management.

As with all mathematical formalizations of aninherently subjective decision-making process, thenumerical answer may not be as important as theprocess itself. The manager evaluation frameworksuggested here is, therefore, analogous to a dis-counted cash flow valuation model for securityselection: The model forces the user to think clearlyabout the validity and iiiternal consistency of his orher assumptions and to communicate thoseassumptions effectively among the user's col-leagues. Although the final manager selection deci-sion may also involve factors not discussed here,the quantitative process of this framework itself isinherently valuable.

Before playing any game, it helps (a lot!) toknow the rules of the game. For the negative-sumgame of hiring fund managers, the rules require atleast two levels of well-above-average skill. As inany game, there will be winners and there will belosers. The good news for those who desire to be

winners is that simply understanding the rules andusing them to guide one's actions can give one atremendous advantage over the competition.

We would Uke to express ou r appreciation to Laurence B.Siegel and Steven Thorley. Their wise commentsandsuggestions helped us to sigiiificantlyimprove this article.

Ttiis article qualifies for 1 CE credit.

Appendix A. The Sponsor'sVersion of the ForecastingEquationAssume we have a set of next-period estimatedz-scores for n fund managers, 2M r(iOlS/w» a'* owhom are under consideration or already employedby the sponsor. These z-scores are unit-normal pre-dictions made by and "owned" by the sponsorabout how good each particular fund manager willbe [here, ZMf(,,) i spon is simplified to 2,,].

Our intention is to use these forecasts to esti-mate the fund manager's actual, realized skill in thenext period, or /C/ ^ (,,) 15 , ,, (simplified here toIC,,). We will tease the required methodology outof the mathematics of regression analysis.

If we regressed the realized information coef-ficients of the managers on the r-scores predictedby the sponsors {we probably would not actuallydo this, but we could), we would be taking advan-

tage of a relationship that has the formIC,^=a + bz,,-\-£^. (Al)

which means that the next-period realized informa-tion coefficient of the fund manager is the value ofthe fitted regression intercept, a, plus the productof the fitted slope, b, times the sponsor's estimatedz-score for the manager, plus or minus an errorterm. If the average information coefficient andaverage z-score are both zero, consistent with ourunderstanding that this is a zero-sum game, then ais also zero; we will make this assumption and willdrop the a term out of the equation.

The regression equation makes obvious theimperfections in the forecast, of course: The real-ized information coefficients will include thispesky error term. But because the error term itselfhas a zero expectancy by construction, we can dropit when considering our best estimate of (or theexpected) information coefficient. With this simpli-fication, we see that the best estimate of the next-period information coefficient of the /;th manageris really simply the slope term, b, times the z-scoregiven the manager:

^C,,=hz^. (A2)

March/April 2008 www.dapubs.org 77

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 14/17

Financial Analysts Journal

We know that th e slope of the regression lineindicated by this value says something about theskill of the sponsor in assign ing 2-scores. We can seethis point more clearly if we decompose the fittedslope term into its natural component terms of cova-riance over variance and then further simplify it:

2

then,

(A3)

{A4)

The first term on the right in Equation A4,

p . 1^- , is the correlation betw^een th e sponsor's

forecast z-scores and the realized information coef-

ficient of the manager, JC,,. In our notation in the

main text, this term is simply th e information coef-

ficient of the sponsor itself, \ 5p,,,, The second

term, a/ - , is also already in our notation as thecross-sectional variation in manager information

coefficient, notated in the main text as a/,^^ ^^^ .

And because z is a norma li zed vari able , a-^ = 1 by

construction, so the final term is simply z,,.

With these understandings. Equation A4 can

be restated in the general form of the familiar fore-

casting equation bu t in a way that reflects its change

in focus from estimating security alphas to estimat-

ing manager information coefficients. Going back

to fully subscripted notation to avoid ambiguity,

we have

^^Mgr\Spon - ^^Spon\Spon^ICMg,.\Spo.,^^^S'^^P""' ( A 5 )

Equation A5 means that the estimated informa-tion coefficient of the manager, in the view of thesponsor, is the information coefficient of the sponsoritself, times the cross-sectional volatilityof managerskill, times the 2-scoreof the manager as estimatedby the sponsor. It is Equation 8 in the main text, afund manager-oriented version of the security-centric forecasting equation (compare with Equa-

tion 6) presented in Grinold (1994) and Grinold andKahn (2000a), both of which are wo rthy of reread ingfor their many w ise insights about alpha.

Notes1. Paraphras ed from ww w.quotationsp age.com; accessedon

11 October 2007.The origin of this quote is not preciselyknown. It has also been attributed to the Danish-Americancomedian and pianist Victor Borge.

2. We use the term "sponsor" throughout,but we mean thearticle to fulty and generally apply to all investors—plansponsors, foundations, endowments, individual investors,and anyone else facing the task of evaluating professionalinvestment fund managers.

3. Specifically, what is needed is an active risk-active returnoptimizer that is capable of running in reverse. See Waringand Siege! (2003).

4. Below-average managers also have someof what wouldordinarily be called "skill" but not enough to be valuable."Skill" in the specialized sense that we use it here is theability to win a zero-sum game.It thus implies an abilitytoadd value, which is not ordinarily something requiredwhen the term is used in other contexts. A below-averagedoctor, for example, is not only skillful but valuable;because he or she is not playing a zero-sum game, anycontribution is a plus. But a below-average active managerhas negative econom ic value. See, for exam ple, Siegei (2004).

5. "Inform ation coefficient"is the preferred term for skill in theliterature of finance; see Grinoldand Kahn (2000a, 2(X)0b).

6. A fund manager who can predict which securities will havenegative alphas and predict what their magnitvide willbealso has skill (a positive information coefficient). This infor-mation is profitable if used as part of the selling disciplineof a long-only manager or for selling short if the fundmanager is allowed to do so .

7. The sp onso r's skill includes the collective skill of the board,staff, and any co nsultants or other advisers used in the fundmanager selection process. Real skillmay exist but bediluted in practice by the governance and decision-making

structure. A sensible effort to reduce that dilution mightinclude a board decision to turn the skill-based decisionsover to professionals on their staffs selected for that skill.

8. In light of the dauntin g odd.sof the game, the reader mightwonder why so many active manager mandatesare stillgranted by plan sponsors. One answer is the pervasivehuman tendency toward overconfidence, which has beenamajor topic amon g behavioral finance researchers. Much ofthe literature on overconfidence proceeds from the obser-vation that trading vo lume is way too highto be explainedby rational models (see, for example, Odean 1998, 1999;Statman, Thorley, and Vorkink 2006). Those w ho choosetoindex are admitting that they possess only average(orworse) skill, and what p lan sponso r is goingto admit that?

9. More precisely, the expectation is that the active managerwill outperform an index fund managed to the same bench-mark after adjustment for the d ifference in fees.

10. This method includes mechanismsfor controlling "misfitrisk." Sponsors generally, and appropriately, imposeanimplied constraint that the sum ofall the sponso r's multifac-tor beta exposures (asset classesand styles, usually), takenacross nil the fund niuiingers am i otiier siibportfolios, must equalthe sponsor's current target asset allocation policy (strategicplus curre nt tactical policy,if any). Misfit risk is the risk thatcomes from violationsof this constraint—an overexposureto value, for example. This constraint is im portantto spon-sors, and to operate underit, fund managers are constrained,in tum, to stay relatively close to their (disclosed) bench-marks. Market-neutral long-short managers, whoseforward-looking benchmarks have zero multifactor betaweights, are also constrained to stay that way, at least onaverage over tim e. Thus, the res ult of anMSO is an optimizedimprovement over the use of simple style boxes, ensuringnot only an op timal trade-off of alpha for expected active riskbut also that the sponsor's benchmark is maintained.

78 www.cfapubs.org ©2008, CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 15/17

Forecastmg Fund Mar^ager Alphas

11 . Numerous stud ies have examined the persistence ofmutual fund performance; see Grinold and Kahn (2000a)for a survey. Although the findings have been mixed,because of differences in study period, time horizon, andmethodology, the correlation between past and future per-formance generally appears to be fairly low. Even optimis-tic studies indicate that the probability of a past winnerremaining a winner is only about 60 percent.

12. The probability levels actually used as boundaries for pass-

ing such a test (or, more properly, for rejecting the nullhypothesis) depend on both the specific type of test and, tosome extent, the judgment of the statistician establishingthe confidence boundaries to be used.

13. Both relationships are also developed in Grinold andKahn (2000a).

14. In this context , by "play often," Grinold and Kahn (2000a,p. 162) mean that the skillful investment manager shouldmake many specific, small, and unrelated bets—not thatthe manager should simply incur high turnover by bet-ting frequently.

15. Clarke, De Silva, and Thorley (2002) developed this impor-tant generalization of efficiency.

16. See Waring and Siegel {2003, Note 25).

17. The authors' colleague and friend Ronald Kahn suggestedthis particular way to combine the two forecasting equa-tions, thereby cleverly and insightfully solving a problemthat we had been working on for some time.

18. One might argue that the mean is not zero for professionalfund managers but possibly positive as a result of a categor-ical difference in skill between individual investors andprofessionals. Waring and Siegel (2003) suggested, however,that if there is such a group effect, it is small, at least in theUnited States, perhaps only 50 bps or so—not enough tooffset fees. Regardless of the argument, if an analyst thinksthat the true mean for the relevant group of professionalfund managers is different from zero, the analyst shouldsimply add the difference to the results from the framework.

19. The exception might be for effects that have not yet beengenerally discovered and that remain unincorporated inprices. Many modern portfolio researchers look for sucheffects. Certain of these researchers may reduce their ideasto computer code (i.e., recipes) in apparent violation of theprescription in the main text. However, the required judg-ment is being exercised when the effect is chosen as a"signal" for the portfolio construction process and eachtime the signal is reviewed for continued inclusion. More-over, over time, most such effects do become known, so the

next opportunity to exercise skill is deciding when toremove a given signal from the overall model. Most com-monly repeated recipes involve well-known ideas and areunlikely to be successful except by chance.

20. By "at the first quartile," we mean at the break point betvi'eenthe top 25 percent of managers and the next 25 percent.

21 . There is nothing special about this number; we are using itsimply as an example. But given typical values for the otherinputs in Equation 11, it is in the right range.

22. In fact, if the sponsor truly has the skill that the board'sdecision to be active presumes, this manner of backing intoan estimate of ^Cs,,,,,, | g,,,,,, will improve the sponsor'sresults. And if the sponsor does not have skill, then theportfolio will be no worse off in expectation than it wouldbe in the absence of the estimate.

23 . Note that the expected win rate only approximates sponsorskill. Consider two sponsors with the identical expectedwin rate; Of the two, the one that overweights the best of itsgood managers clearly has more skill than the one thatassigns them all equal weights (the sponsor gets value fromestimating not only the sign of the manager's performancebut also the magnitude). Regardless, using the expected winrate should provide estimates of the information coefficientthat are in the right ballpark.

24. Fees are the only component of alpha that one can know forcertain, and the fee amount does not require any estimateof sponsor skill.

25. The term "actively evaluated" keeps the emphasis on thenumber of securities that the manager follows and couldpotentially hold rather than on the number of securitiescurrently in the portfolio. Thenumber in the portfolio mightunderestimate breadth because a manager might omit asecurity from the portfolio simply to reflect a negative view.

26. Carrying out some sort of style analysis on fund managerswill generally be better than using a simple benchmarkwhen separating alpha from beta. The biggest exception isfor style rotators, tactical asset allocators, and those whosestyles are themselves the subject of intentional active bets

and thus not stable over time. In such cases, style analysismay not effectively add to one's knowledge of the fundmanager's beta. Regression is not powerful enough in thepresence of time-varying beta bets. Other means, usuallysubjective, must be used.

27. Of course, an ail-seeing sponsor would pick a better man-ager if the case gave the sponsor a richer sample to choosefrom; this manager is barely top quartile.

ReferencesClarke, Roger, Harindra de Silva, and Steven Thorley. 2(X)2.

"Portfolio Constraints and the Fundamental Law of Active Man-agement." Financial Anali/$ts Joimml, vol. 58, no. 5 (September/

October):48-66.

Grinold, Richard C. 1989. "The Fundamental Law of Active

Management." Journal of Portfolio Maimi^cmeitt, vol. 15, no. 3(Spring):30-37.

• , 1994. "Alpha Is Volatility Times /CTimes Score." Journalof Portfolio Miimigcnumt, vol. 20, no. 4 (Summer) :9-l 6.

Grinold, Richard C, and Ronald N. Kahn. 2000a. Active PortfolioManagement. 2nd ed. New York: McGraw-Hill.

. 2000b. "EfficiencyGainsof Long-Short Investing." Finan-tf^ Journal, vol. 56, no. 6 (November/December):40-53,

Kahn, Ronald N. 2000. "Most Plan Sponsors Need More En-

hanced Indexing." In Enhimced Indexing: New Strategia^ an d Tech-niques for Investors. Edited by Brian R. Bruce. New York:Institutional Investor.

Odean, Terrance. 1998. "Volume, Volatility, Price, and ProfitWhen All Traders Are Above Average." Journal of Finance, vol. 53,no . 6 (December): 1887-1934.

. 1999. "Do Investors Trade Too Much?" AuiericanEconomic Review, vol. 89, no. 5 (December):1279-1298.

Sharpe, William F. 1991. "The Arithmetic of Active Manage-ment." Financial Anah/sts Jouriini, vol. 47, no. 1 (January/February): 7-9.

Siegel, Laurence B. 2004. "Distinguishing True Alpha fromBeta." In Points of Inflection: New Directions for PortfolioManagement. Charlottesville, VA: CFA Institute:20-29.

March/April 2008 www.cfapubs.org 79

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 16/17

Financial Analysts Journal

, Meir, Steven Thorley, and Keith V orkink.2006. "Inves-tor Overconfidence and Trading Volume."Rcvkiv ofFinancialStudies, vol. 19, no. 4 (Winter): 1531-1565.Waring, M. Barton, and LaurenceB. Siegel. 2003. "Understand-ing Active Management." hwestment Insights,vol. 6, no . 1(April):3-41. Republished in two parts as "The Dimensions ofAct ive Management ," journal of Portfolio Management, vol. 29,

no. 3 (Spring 2OII3):35-51, and "Deb unking Some M ythsofActive Management,"joiirunl ofhwesting, vol. 4, no . 2 (Summer2005):20-28.Waring, M. Barton, Duane Whitney, John Pirone, and CharlesCastille. 2000. "Optimizing Manager Structure and BudgetingManager Risk ." journal of Portfolio Management, vol. 26, no. 3

(Spring) :90-94.

Reach leadinginvestment

professionals atfinancial institutions

across the globe.

To advertise, please contact Jenine Kaznowski-M {434)951-5386

A Pttbllnthin of CM [IMUI

80 www cfapubs org ©2008 CFA Institute

8/6/2019 Waring 2008 Portfolio Construction

http://slidepdf.com/reader/full/waring-2008-portfolio-construction 17/17